Global Wind Report 2022

The wind industry enjoyed its second-best year ever amidst pandemic but new installations must still quadruple by the end of the decade to meet a net zero pathway.

Key Highlights

- The global wind industry had its second-best year in 2021, with almost 94 GW of capacity added globally, trailing behind the 2020’s record growth by only 1.8%.

- Europe, Latin America and Africa & Middle East had record years for new onshore installations, but total onshore wind installations in 2021 was still 18% lower than the previous year. The decline was driven primarily by the slow-down of onshore wind growth in the world’s two largest wind power markets, China and the US.

- 21.1 GW of offshore wind capacity was commissioned last year, three times more than in 2020. making 2021 the best year in offshore wind history, bringing its market share in global new installations to 22.5% in 2021.

- China made up 80% of offshore wind capacity added worldwide in 2021, bringing its cumulative offshore wind installations to 27.7 GW. This is an astounding level of growth, as it took three decades for Europe to bring its total offshore wind capacity to a similar level.

- Total global wind power capacity is now up to 837 GW, helping the world avoid over 1.2 billion tonnes of CO2 annually – equivalent to the annual carbon emissions of South America.

- Wind auction activities bounced back in 2021 with more than 88 GW of wind capacity awarded globally, 153% higher than in 2020.

- After a year in which net zero commitments gathered global momentum, coupled with renewed urgency for achieving energy security, the market outlook for the global wind industry looks even more positive. 557 GW of new capacity is expected to be added in the next five years under current policies. That is more than 110 GW of new installations each year until 2026.

- However, this growth needs to quadruple by the end of the decade if the world is to stay on-course for a 1.5C pathway and net zero by 2050.

Lagging growth will leave a wind energy shortfall by 2030 without action

Wind energy is not growing nearly fast or widely enough to realise a secure and resilient global energy transition. At current rates of installation, GWEC Market Intelligence forecasts that by 2030 we will have less than two-thirds of the wind energy capacity required for the 1.5°C and net zero pathway set out by IRENA in their 2050 roadmap, effectively condemning us to miss our climate goals.

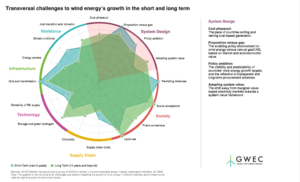

Six areas the global wind industry faces challenges in the short and long term

Wind energy’s role as a protagonist of the energy transition will depend on ensuring the industry’s growth is sustainable, just and socially responsible, while resting on a clear and viable economic proposition. There are six areas the industry faces both short and long term challenges.

Source: GWEC